ShareIn's response to FCA Discussion Paper DP25/3

Dr. Tania Wood, Head of Compliance, ShareIn

The FCA's Discussion Paper DP25/3: Expanding Consumer Access to Investments is asking the right questions. Enabling more consumers to invest, with appropriate information and protection, is genuinely important — and we support the direction of travel.

But there's a structural problem sitting underneath all of it that the paper doesn't quite name directly. The current retail investment framework treats a secured loan to a solar project in the same regulatory bucket as a leveraged cryptoasset derivative. That's a category error, and it's causing real damage — to borrowers, to platforms, and to the investors the rules are meant to protect.

The conflation problem

Under the current COBS 4 architecture, Restricted Mass Market Investments (RMMIs) and Non-Mass Market Investments (NMMIs) sweep up products with fundamentally different risk profiles. Leveraged derivatives, highly volatile speculative instruments, and unleveraged loans to asset-backed SMEs all end up in similar regulatory territory.

A secured loan to a community renewable energy project with contracted revenues is not structurally equivalent to a leveraged meme-coin derivative. Treating them as if they are doesn't protect consumers — it just creates friction in places where it doesn't belong.

Illiquidity is the thing these products share. But illiquidity on its own tells you almost nothing useful about the real risk to a consumer. Whether something is volatile, leveraged, speculative, or structurally engineered to amplify losses — those are the dimensions that actually matter for consumer protection.

What the friction looks like in practice

ShareIn builds infrastructure for FCA-regulated crowdfunding platforms. We see both sides of the market — investors coming in, and borrowers raising capital. The data on what the current regulatory burden actually does to participation is not pretty.

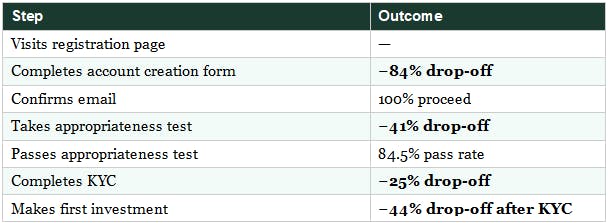

On the investor side: fewer than 6% of prospective investors who reach the registration page go on to make a first investment. The new investor funnel breaks down like this:

This level of attrition is not a sign that the framework is successfully filtering out unsuitable investors. The people falling out at the appropriateness test and KYC stages are largely people who wanted to invest in community solar and SME lending — not gamblers looking for leverage. The friction is in the wrong places.

On the borrower side, the picture is even starker. Average staff hours to onboard a single borrower: 277 hours — and that's true even for repeat borrowers who've been through the process before. Three-quarters of prospective borrowers drop out during the compliance phase entirely. In many cases, the cost of onboarding approaches or exceeds the arrangement fee revenue the transaction generates.

Smaller borrowers — community enterprises, local renewable projects, SMEs without dedicated finance teams — are simply not willing or able to run that gauntlet. Some raise money through unregulated channels instead. The regulation meant to protect investors ends up pushing activity outside the perimeter where there's no protection at all.

The FOS liability problem

The financial promotion rules under COBS 4.12A and COBS 4.12B require that promotions be fair, clear, not misleading, and reasonably capable of achieving the advertised return. That's the right principle. But the way it interacts with FOS redress creates a problem that's hard to overstate.

If a borrower underperforms commercially, an investor may complain to the Financial Ombudsman Service. If that complaint is upheld, the platform can be required to repay full invested capital plus 8% statutory interest. The platform didn't manufacture the product. It doesn't control whether a solar installation gets built on time, or whether a small business has a difficult year. But it carries the redress risk regardless.

The rational response to that liability is defensive over-collection of borrower information, conservative approval decisions, and higher costs for everyone. Smaller borrowers get screened out not because they're unsuitable, but because the downside risk of approving them is asymmetric. This isn't a failure of individual platforms — it's a predictable consequence of how the rules currently work.

Our proposal: the PIRI category

We're proposing that the FCA introduce a new regulatory category: Productive Illiquid Retail Investments, or PIRI.

The defining characteristics would be:

- Capital deployed to identifiable productive economic activity

- Typically debt or equity in SMEs or community enterprises

- Unleveraged — no embedded derivative amplification

- Medium-term and illiquid by nature

- Not structurally engineered to amplify volatility

- Fundamentally distinct from speculative or synthetic instruments

The point isn't to create a lighter-touch regime for its own sake. It's to match the regulatory treatment to what the actual risks are. A PIRI classification would mean standardised illiquidity warnings (illiquidity is a real risk — investors should understand it clearly), appropriateness testing calibrated to the actual product type rather than crypto-level standards, and due diligence guidance that gives platforms clarity about what's expected of them.

At the moment, platforms operate under genuine uncertainty about where the line is between appropriate due diligence and over-collection. That uncertainty is expensive, and it gets passed on to borrowers and ultimately to investors.

The broader picture

Crowdfunding infrastructure plays a real role in financing renewable energy installations, community enterprises, and SMEs that wouldn't otherwise have easy access to capital. The over-deterrence created by the current framework doesn't just affect platforms and their customers — it conflicts with the UK's sustainable finance agenda and its stated growth objectives.

The FCA has a secondary objective to support competition and growth. We'd argue this is precisely the kind of situation that objective was designed to address.

What we're asking for

Our submission to DP25/3 makes four concrete asks:

- Introduce the PIRI category — or a functionally equivalent mechanism — to decouple productive illiquid investments from genuinely high-risk complex products

- Provide clear, risk-based guidance on financial promotion due diligence expectations, including where the boundary sits between borrower commercial risk and platform disclosure liability

- Clarify how financial promotion standards interact with FOS redress, so platforms aren't forced to assume worst-case liability on every decision

- Align appropriateness testing with the actual risk profile of the product — not with frameworks designed for leveraged derivatives

We also support a broader shift from product-label categorisation to a genuinely multi-dimensional risk framework — one that looks at leverage, volatility, liquidity, counterparty exposure, asset backing, and economic substance together. Return potential alone is not a reliable proxy for structural risk, and the framework should reflect that.

Relevant links

FCA Discussion Paper DP25/3: Expanding Consumer Access to Investments

COBS 4.12A — High-risk investments: specific requirements (RMMI)

COBS 4.12B — Non-mass market investments (NMMI)

ShareIn Ltd is FCA authorised (FRN 603332). If you'd like to discuss any of the issues raised in this piece, get in touch.